The Investor's Briefing #11

Trade War Reignited?, Apple Shifts Focus, Axon Deep Integration and Drones

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the eleventh edition of our weekly newsletter: The Investor’s Briefing.

In Financial News.

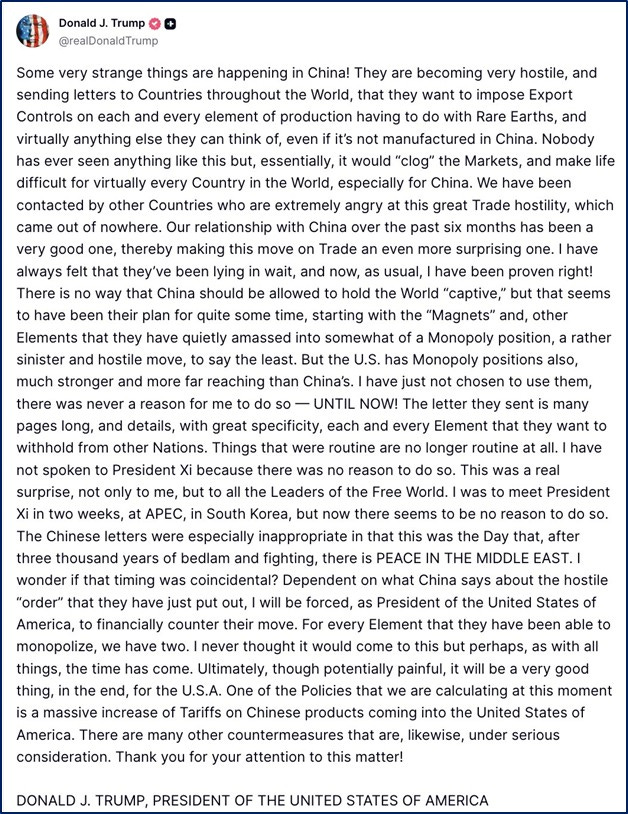

Markets reversed early gains Friday after President Trump said he may cancel a planned meeting with China’s president and is considering “a massive increase in tariffs” on Chinese goods, rekindling fears of renewed trade tensions between the world’s two largest economies.

The Nasdaq fell about -3.5%, while the S&P 500 lost -2.7% after fluctuating earlier in positive territory. The sell off followed a post by the President on Truth Social, in which he accused Beijing of becoming “very hostile” and warned that China was preparing broad export controls on rare earth elements and other industrial inputs. “Nobody has ever seen anything like this,” Trump wrote, claiming such measures could “clog markets and make life difficult for virtually every country in the world.”

Average U.S. tariffs on Chinese goods currently stand near 57%, according to the Peterson Institute for International Economics, down from more than 140% at the peak of the trade tensions earlier this year. Trump’s latest comments signal a renewed escalation with a threat of additional 100% tariff. “I was to meet President Xi in two weeks, at APEC, in South Korea, but now there seems to be no reason to do so,” he wrote.

The comments immediately rippled through equity markets, with U.S. semiconductor stocks leading declines. AMD dropped -7%, Broadcom slid -5%, and Qualcomm lost -6% after reports that Beijing had launched an anti-monopoly investigation into the company. The renewed volatility underscores how sensitive the technology sector remains to shifts in U.S.–China policy, particularly around trade and supply chains for advanced chips.

Earlier in the day, Chinese equities had already weakened as Beijing escalated its own pressure campaign. Authorities introduced new rare-earth export restrictions, imposed a special port fee on U.S. vessels, and signaled further scrutiny of American tech firms. Analysts said the measures reflect China’s willingness to use economic leverage as trade negotiations stall.

Friday’s retreat erased the week’s earlier gains across major indicies and represents the largest sell off since the orginal tariffs were announced in April.

Company News.

Axon Executive on Evidence.com Advantage and Drones (Alphasense Expert Call)

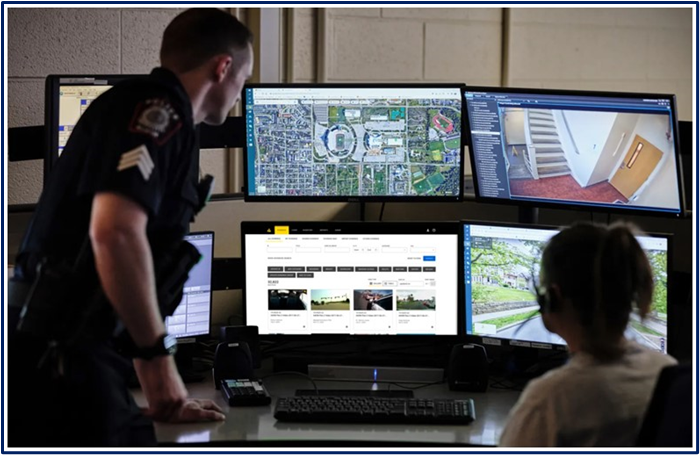

A former Axon executive described Evidence.com as one of the company’s most defensible assets, rating it “a seven or eight out of ten” in terms of difficulty to replicate. While its interface looks similar to other evidence management systems, Axon’s real advantage lies in its deep customization options, rich metadata architecture, and growing network effects across law enforcement and prosecutors.

“At face value, it’s nothing to write home about, but Axon can configure it deeply around agency policy, by role, badge number, or location, automating permissions at implementation.”

Switching to another provider is extremely difficult. The average agency stores between 60 terabytes and several thousand terabytes of footage on Azure servers. Transferring that data is not only time-consuming but also risks losing hundreds of unique metadata fields. Beyond basic information like timestamps or resolution, Axon’s videos contain GPS coordinates, movement tracking, AI-generated tags, and redaction markers, all of which are lost outside the Axon ecosystem.

“If you move away, all you’re left with is the core video. For most agencies, that’s not enough to prosecute.”

Evidence.com supports roughly 98% of all video formats and can also store audio from interviews and interrogations. Many agencies use it for all forms of digital evidence because of its secure chain of custody and detailed audit trails that confirm files haven’t been altered.

Turning to competition, they note that Motorola Solutions, through its WatchGuard acquisition, remains Axon’s main competitor. Motorola offers comparable storage and sharing features, but lacks Axon’s automation and AI-driven tools such as automatic redaction, transcription, and report writing.

When this expert left Axon (Summer 2023), the company controlled roughly two-thirds of the evidence management market, with Motorola capturing most of the remainder. Where Motorola still holds customers, it’s usually because of long-term contracts or inertia, not better technology.

“In law enforcement, if something works, they keep it for 20 years… Axon just waits for the renewal window.”

The expert acknowledged that some agencies worry about relying too heavily on a single vendor but said price is the more common limitation, “They trust Axon, they just can’t always afford Axon.” The executive believes Axon’s AI advantage will continue to strengthen as the company collects more data. “The provider with the most history to draw upon will build the best models,” he noted. Still, the expert sees the next major opportunity not in AI but in drones.

“If Axon can make the drone market affordable and scalable, that’s how they reach another level of profitability. AI will become standard, drones are the next real differentiator.”

Axon initially partnered with Flock Safety before developing its own competing solution. However, the excutive expects Flock to remain a strong number-two player, but believes Axon will lead the market due to its “deep R&D investment and strong customer feedback loop.”

In summary, the executive believes Axon’s Evidence.com remains a core advantage, reinforced by scale and integration. However, he believes the next phase of growth will depend on the company’s ability to execute in drones and real-time situational awareness, rather than incremental AI improvements.

This is from an AlphaSense Expert Call Interview.

You can get a free trial of AlphaSense here

AXON 2Q25 Business Update

Apple Shifts Focus From Vision Pro to Smart Glasses in a Bid to Catch Meta

Apple is redirecting resources away from a planned overhaul of its Vision Pro headset to accelerate development of smart glasses, underscoring a strategic pivot toward wearable devices it sees as more commercially viable. The move reflects both disappointing consumer adoption of the Vision Pro and intensifying competition from Meta in the fast-emerging smart glasses market.

Apple had been preparing a cheaper, lighter version of the Vision Pro (code-named N100) for release in 2027. However, the company recently paused that effort and reassigned engineers to focus on glasses development. The shift comes after the Vision Pro’s lackluster reception. Priced at $3,499, the headset has been criticized as heavy and costly, while also suffering from limited video content and apps. Apple still intends to release a modest refresh of the current Vision Pro later this year with a faster chip.

In place of the scrapped update, Apple is advancing at least two glasses projects. The first, N50, will pair with an iPhone and lack its own display. Apple aims to preview this model as early as next year, ahead of a planned 2027 release. A second version, equipped with an integrated display, is also in development. Initially targeted for 2028, that timeline is now being accelerated as Apple seeks to respond to Meta’s newly launched Ray-Ban Meta Display glasses. Apple’s glasses are expected to feature speakers for music playback, cameras for recording, health-tracking capabilities, and a new custom chip, with designs offered in multiple styles.

However, Apple faces hurdles on the software side. Apple’s Siri voice assistant continues to lag rivals, and its broader Apple Intelligence platform only began rolling out this year. To address these weaknesses, Apple is working to rebuild Siri with a targeted for release as early as March 2026, which is expected to anchor the new device line.

Apple’s pivot also highlights its relative position behind Meta. Meta introduced its first Ray-Ban smart glasses in 2021, followed by a 2023 update that gained traction with consumers. This year, it launched a $799 display-equipped model that has generated strong early interest and refreshed its non-display line with improved cameras, longer battery life, and designs tailored for athletes. Meta is also developing a follow-up display model for 2027 with dual lenses, allowing information to be shown in both frames. By contrast, Apple’s progress with enclosed mixed-reality headsets has been slower, with Vision Pro adoption falling short and marketing increasingly targeted toward enterprise users, a path previously taken by Microsoft and Google with limited success.

The competitive landscape is broadening further though. Amazon and Google are pursuing their own AI-enabled wearables, while OpenAI has enlisted former Apple design chief Jony Ive to help develop a suite of AI-powered devices. Within this context, Apple faces mounting pressure to demonstrate leadership after spending more than a decade and billions of dollars developing the Vision Pro.

Even so, Apple has not completely abandoned headsets. It continues to plan incremental Vision Pro updates, and could ultimately revisit a lighter, lower-cost version. After shelving not only the N100 project, but also earlier tethered AR glasses (code-named N107) that were designed as external displays for Macs, Apple’s immediate priority is clear: find product-market fit for a smart glasses device.

Success will depend on whether Apple can close the gap with Meta and overcome its own shortcomings in AI and voice interaction. For now, the company is signaling to investors and consumers alike that glasses, not headsets, are more likely to define the next era of personal technology.

Equifax Cuts Mortgage Credit Score Prices After FICO Redraws Market Model

Equifax is lowering the price of its mortgage credit scores in response to a major competitive shift by Fair Isaac (FICO), which has begun selling scores directly to mortgage resellers, a move that threatens to upend a decades-old industry structure.

Equifax said Tuesday it will offer its VantageScore 4.0 mortgage credit scores for $4.50 through the end of 2027, less than half of the $10 price FICO set for 2026. The announcement follows FICO’s decision to bypass traditional credit bureaus and sell directly to lenders and intermediaries.

For more than three decades, FICO scores have served as the benchmark for credit risk in U.S. consumer lending. First introduced in 1989, the metric became deeply embedded in the mortgage market after Fannie Mae and Freddie Mac adopted it as a requirement for loan evaluations. Historically, lenders accessed these scores through the three nationwide credit-reporting agencies, Equifax, Experian, and TransUnion, which bundled FICO scores with borrowers’ credit files.

FICO’s new program allows mortgage resellers to calculate and distribute scores themselves, eliminating the credit bureaus as intermediaries. The company said the change aims to increase transparency and reduce costs for lenders, brokers, and other market participants. Analysts noted that by capturing distribution revenue directly, FICO could meaningfully improve profitability and tighten its control over how scores are deployed across the lending ecosystem.

In turn, Equifax has responded with aggressive pricing and new incentives. CEO Mark Begor said the company believes “open competition” is the best path to lower costs and greater access. “Equifax plays an essential role in the financial lives of consumers and the mortgage industry,” Begor said. “We take that responsibility seriously—particularly in the most challenging mortgage and housing market in 20 years.”

Alongside the price cut, Equifax said it will offer free credit scores to all of its mortgage, automotive, card, and consumer finance clients who purchase FICO scores through the end of 2026. The company added that it aims to make VantageScore 4.0 more widely accessible, emphasizing its use of alternative data, such as rental and utility payment histories, often missing from traditional credit reports.

The decision highlights how the once-stable credit scoring industry is entering a more competitive phase. With mortgage volumes constrained by high interest rates and lenders under pressure to manage costs, both FICO and the credit bureaus are positioning for advantage in what could become the most consequential shift in mortgage credit assessment in a generation.

We changed up the format of the company section to extend the story of each company. If you enjoyed this, please drop a comment or like so we know to keep doing it in the future! Feedback is always welcomed.

Spotlight.

This week, we released our exploratory report of Casey’s! Casey’s unique model relies on a fresh food offering to differentiate themselves from an otherwise commoditized business. They are the 5th largest pizza retailer and have over 9 million loyalty members. Similar to Dollar General, they operate primarily in small towns with populations of 500-20k people. They currently trade at about a 21x free cash flow multiple and intend to grow EBITDA 8-10% overtime. Learn more about Casey’s here!

As the 3Q earnings season starts in the coming weeks, check out all of our 2Q25 business updates we have released to stay up to date.

2Q25 Business Updates: Meta, Copart, APi Group, Floor & Decor, AppFolio, Coupang, Axon, Airbnb, Evolution, CoStar Group, Perimeter Solutions, Constellation Software, RH, and DFH.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

PRM 2Q25 Business Update

Perimeter Capital Allocation: “Their capital allocation continues to be superb. Perimeter deployed approximately $62mn in capital during the quarter. They invest into 3: internal capex, stock repurchases, and M&A, all of which they expect to generate a 15% or higher return on. Organic investments included $12.8 million in capital expenditures, primarily tied to production expansion in Fire Safety and Specialty. They repurchased 2.9 million shares for roughly $32 million, noting that they only opportunistically repurchase shares when they see a 15%+ IRR.”

Perimeter 2Q25 Business Update

Interview. Head of M&A at CSU on Copycats

CSU’s Advantage Over Copycats: “What does the copycat bring to the table that Constellation doesn’t already have? Constellation has the capital, it’s a more disciplined acquirer. Constellation holds a tremendous advantage over the copycats in the sense that it’s got an unparalleled depth of expertise in terms of its internal network of operators and knowledge.”

Listen to the full interview here 👇

The Synopsis Podcast.

This week, we released a dialogue episode on Meta’s new Vibes product and read into what OpenAI’s introduction of instant checkout can mean for the future of the internet. Listen below!

Memo of The Week.

Investing is Just Answering a Series of Questions: Explaining the Reverse DCF

“Investing is just asking a series of questions and seeing what the associated payoffs are if that scenario materializes. This is the beauty of a Reverse DCF. Instead of us picking specific growth rates and a discount rate that spits out a stock price value, we invert the process. We start with the current stock price and then sensitize around a range of assumptions (like revenue growth and margin for example). The output of the Reverse DCF is the discount rate that sets our DCF model equal to the current market value (or enterprise value). This effectively allows us to see what return an investor can expect for making different assumptions. We want to know that if we assume a very high growth rate (which should be considered riskier) that the return we calculate is compensatory for that scenario. Conversely, if we use very conservative assumptions, we may want to see that we are at least clearing the risk-free rate.”

Learn more about your true cost of equity in this memo here 👇

Investing is Just Answering a Series of Questions: Explaining the Reverse DCF

Company Report Snippet: Casey’s (CASY)

Casey’s Unique Offering: “Surprisingly, 75% of Casey’s purchases do not include fuel. The lack of reliance on these categories for sales suggests that Casey’s has a unique offering in their made-to-order food and general merchandise, which draws customers in without the need for these other traffic drivers. However, a unique offering should not be confused for a defensible offering. Casey’s food and general merchandise items are unique and generate higher margins largely because of the lack of competition in a given town”.

*This is an excerpt from our company report on Casey’s.

If you are a Speedwell Research Member, read the full report here: Casey’s

If you are not already a Speedwell Research member, you can purchase it here: Casey’s Individual Report

Upcoming.

Research

Current research report in progress: Shift4, the payment provider. Shift4 caught our attention because it is in a generally sticky industry (payments + software), still has founder involvement, is growing topline over >20%, and is down -35% from peak. Stay tuned for more!

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Stan Druckenmiller and Jeff Feig (2009) (link)

Liberty: Interview with Ho Nam of Altos Ventures (link)

Aswath Damodaran: A “Fairly Highly Valued” Market (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).