The Investor's Briefing #6

Google's TPUs challenge Nvidia's GPUs, Apple's Antitrust Relief, Soft Labor Markets Embolden Rate Cut Expectations

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the sixth edition of our new weekly newsletter: The Investor’s Briefing.

In Financial News.

U.S. markets advanced to fresh highs as cooling labor market data reinforced expectations of rate cuts and Google’s antitrust victory added momentum to the technology sector. The week also brought historic pledges from top tech executives to boost U.S. AI infrastructure investment, underscoring the intersection of policy, regulation, and corporate capital allocation.

Earlier in the week, the Google antitrust case concluded with a federal judge ruling that Google does not have to sell or divest its Chrome browser (nor Android), despite the Department of Justice’s allegations that Google’s market share in search and browsers constituted an illegal monopoly. U.S. District Judge, Amit Mehta, decided against the DOJ’s request for Google to be forced to sell off Chrome or break up its business, judging such an action as too extreme for the facts of the case. In the case he alluded to the increase in competition from AI chatbots as a reason to let the market sort itself out.

Furthermore, Alphabet will be allowed to continued to make payments to Apple through their revenue share agreement, which is no doubt a huge relief to Apple. We estimate that these so called Traffic Acquistion Cost (or TAC) payments represent 20-25% of Apple’s EBIT. However, it was also ruled that to remedy past anti-competitve behavior, Alphabet will have to give competitors one-time access to their search index. Alphabet plans to file an appeal. Alphabet and Apple shares rallied +9% and +5%, respectively, after the ruling, and lifting both the S&P 500 and Nasdaq to new all-time highs. However, the S&P 500 finished the week -12bps, with the Nasdaq +32bps.

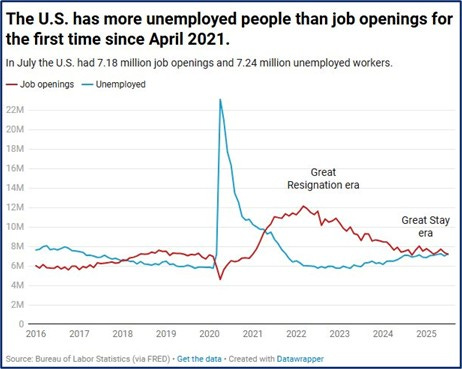

Turning to the labor market, the July Job Openings and Labor Turnover Survey (JOLTS) reported further signs of labor market weakness. Job openings fell to 7.2 million in July, a decline of -176,000 from June and the lowest level since September 2024. For the first time since April 2021, there were more unemployed workers than available positions, with just 0.99 job openings per job seeker.

During much of the post-pandemic recovery, openings consistently outpaced the number of unemployed people, peaking at nearly 2-to-1 in early 2022. This reversal marks a significant cooling in labor demand and highlights the erosion of one of the labor market’s strongest supports over the past three years.

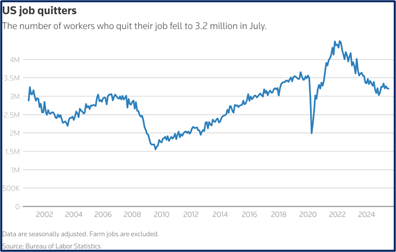

Meanwhile, the national quit rate held steady at 2.0%, reflecting increased worker caution as job security concerns rise alongside persistent living cost pressures. By comparison, the quit rate peaked at 3.0% in late 2021 and early 2022 during the “Great Resignation,” when workers were confident in switching jobs for higher pay. The current level marks a return to pre-pandemic norms, underscoring how employee bargaining power has weakened as the labor market cools.

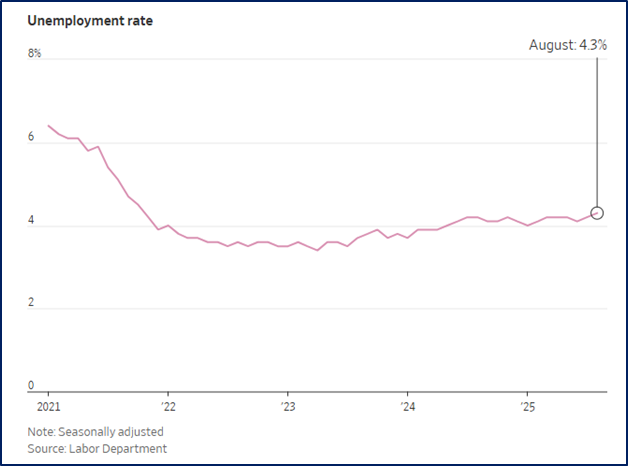

On Friday, the latest jobs report was released. The report showed that U.S. job growth slowed further in August as nonfarm payrolls increased by just +22,000, well below the +75,000 expected, reinforcing signs of labor market softness. The Labor Department also revised its numbers from June, and stated that the U.S. lost -13,000 jobs, which was the first decline since December 2020. The unemployment rate edged up to 4.3% from 4.2% in July. The data underscored mounting weakness in employment conditions and strengthened the case for a 25 bps rate cut by the Federal Reserve later this month. Markets responded positively: equities and bonds rallied, while U.S. Treasury yields fell to five-month lows, with the 2-year yield declining 11 bps to 3.48%.

President Trump hosted top tech leaders at the White House, including Tim Cook, Mark Zuckerberg, Bill Gates, Sundar Pichai, Sam Altman, and Satya Nadella, in a show of support for U.S. technology and AI leadership. Executives detailed multibillion-dollar commitments to domestic data centers and infrastructure. Zuckerberg pledged at least $600 billion through 2028, while Cook reaffirmed Apple’s $600 billion U.S. manufacturing investment. Both cited administration policies as catalysts.

These announcements build on a broader wave of corporate promises secured by the White House as companies seek to expand U.S.-based capacity while avoiding tariffs on imported semiconductors and AI hardware. The focus on domestic infrastructure underscores Washington’s intent to maintain a technological edge over China and meet the surging energy and computing demands of artificial intelligence.

Company News.

Google, one of the largest buyers of Nvidia AI chips, is ramping up efforts to grow its own AI chips, called Tensor Processing Units or TPUs. TPUs are Google’s in-house chips, purpose-built for deep learning to deliver superior efficiency and lower cost at massive scale, but they lack the flexibility of general-purpose GPUs and are difficult to deploy outside the Google Cloud ecosystem.

In a first-of-its-kind move, Google struck a deal with London-based Fluidstack to place TPUs in a New York data center, marking the first time its custom chips will be hosted by another cloud provider. The strategy directly challenges Nvidia’s stronghold, as many smaller providers currently rely soley on Nvidia GPUs. With AI developers eager to diversify from a single supplier, Google is positioning TPUs as a competitive alternative.

As many investors know, it is Nvidia’s CUDA software platform that protects their GPUs against potential competitors. More than 4 million developers use CUDA to accelerate workloads on Nvidia GPUs, creating a powerful ecosystem lock-in beyond their raw hardware. Within GPU programming, CUDA commands the overwhelming majority of developer adoption.

In contrast, Google’s TPUs are accessed primarily through TensorFlow and JAX, which compile workloads via Google’s XLA compiler. While TPUs can deliver performance that rivals Nvidia GPUs, the smaller base of developers trained to optimize for TPUs has constrained broader adoption.

One open question is whether advances in AI could eventually translate CUDA-based code into TPU-optimized instructions. Today, any such translation is error-prone and requires significant debugging, offsetting potential performance benefits. But in the long run, if AI compilers could automatically port CUDA kernels into TensorFlow/XLA or JAX with high reliability, it could erode Nvidia’s network effect advantage in software.

However, it is still true today that all major AI frameworks such as PyTorch and TensorFlow are optimized for CUDA first, meaning new models and research generally run on Nvidia GPUs out of the box — further reinforcing Nvidia’s software moat.

Still, if AI translation matures to the point of seamless interoperability across hardware, it could represent one of the few credible threats to Nvidia’s current dominance. The core of Nvidia’s moat is not just silicon performance but the switching costs embedded in CUDA’s developer ecosystem. If AI compilers reach a stage where CUDA code can be reliably translated into frameworks that run efficiently on alternative hardware — such as TPUs or even AMD GPUs — the friction that locks developers into Nvidia would diminish. Theoretically, hardware choice would tilt more toward price-performance and availability rather than software compatibility.

Such a shift would be profound: it would reduce the “tax” of rewriting and debugging CUDA-specific code, potentially opening the door for hyperscalers (Google, Amazon, Microsoft) or new chip entrants to compete on more equal footing. While this scenario is far from imminent, it highlights that Nvidia’s long-term risk is less about competitors building better chips and more about competitors breaking CUDA’s software monopoly through interoperability.

Salesforce shares fell ~7% after guiding 3Q revenue to $10.2bn–$10.3bn, signaling muted growth despite AI investments. Adoption of its Agentforce AI tool is rising, with customers moving from pilot to production up +60% q/q, but revenue impact remains limited. The slow ramp underscores concerns that incumbent SaaS firms face mounting pressure from AI-native rivals, and questions the durability of per-user subscription models. Salesforce expanded its buyback program to $50bn and reaffirmed plans to acquire Informatica in early 2026, but investors remain cautious until AI contributions drive meaningful top-line growth. CRM trades at 37x earnings with LTM revenues growing 8%.

Broadcom shares rose after reporting strong quarterly results and issuing upbeat guidance for its AI chip business. The company announced a $10 billion partnership with OpenAI to design and manufacture the startup’s first custom AI chip, expected next year. The deal reflects OpenAI’s long-term strategy to diversify beyond Nvidia GPUs, while positioning Broadcom as a key player in the race to build specialized AI hardware. Their XPU chip, like Google’s TPU, is purpose-built for AI, but aims to offer broader flexibility and higher scalability—combining efficiency with the ability to handle diverse workloads at hyperscale.

Broadcom CEO Hock Tan on demand for custom AI accelerators said: “Now let me give you more color on our XPU business which accelerated to 65% of our AI revenue this quarter. Demand for custom AI accelerators from our 3 customers continue to grow as each of them journeys at their own pace towards compute self-sufficiency.”

Lululemon shares fell -17% after reporting earnings on Thursday. The company grew revenues +7% y/y to $2.5bn, but North America same store sales fell -4%. Driving the stock lower was a guidance cut, weak U.S. sales, and rising cost pressures from tariffs. While management noted they missed with some of their product selections, investors are wondering to what extent competition from the likes of Alo, Vuori, and others are weighing on the athleisure retailer. Shares trade at just 14x earnings.

Lululemon CEO on why U.S. growth has stalled: “The competitive landscape is different today than it was even 2 or 3 years ago. And while no single competitor is having a meaningful impact on our business, there are now many players in the market… The primary cause is that we relied too heavily on some of our core franchises across lounge and social for too long. We did not have the appropriate balance between existing and new styles across our casual offerings and the guests stopped responding as they had in the past.”

American Eagle saw its revenue dip by -1% to $1.3bn but delivered a +15% EPS growth. Shares rallied as much as 38% in the days following these results, fueled by better-than-expected profits, upbeat guidance for the second half of the year, and the brand’s innovative celebrity marketing campaigns featuring Sydney Sweeney and Travis Kelce, which drove over 700,000 net new customer acquisitions and increased brand engagement across both men’s and women’s categories.

CEO Jay Schottenstein on increase traffic from marketing campaigns: “Sweeney Signature jeans sold out within a week and some products within 1 day. Demand for her curated online shop has been very strong...We are off to a start beyond our wildest dreams.”

Tesla proposed a new pay package for CEO Elon Musk that could be worth over $1 trillion over the next ten years. The proposal would increase Musk’s stake in Tesla to as much as 29% if all of the targets are met. Under the new plan, Musk has to hit 12 market cap, in addition to 12 operational milestones, such as delivering 20mn Tesla vehicles, 1mn Optimus robots, 1mn robotaxis in operation, and growing adjusted EBITDA to $400bn (Tesla reported $16.6bn in adj. EBITDA. in 2024). The maximum payout is contingent on Tesla reaching a market cap of $8.5 trillion. Tesla shareholders are set to vote on this proposal in early November.

C3.ai, an enterprise software company that helps organizations deploy AI solutions to boost efficiency and cut costs, reported 1Q26 and revenues fell -19% y/y. This was well below analyst expectations, triggering a -12% share price decline. Net losses widened, and next-quarter guidance came in ~25% below Wall Street forecasts, amplifying concerns over the company’s ability to convert AI adoption into sustainable revenue growth. The results mark a sharp reversal from 2Q25, when revenue climbed +29% y/y on the back of Microsoft partnerships and enterprise demand. The downturn reflects a broader market reality: investor enthusiasm for the “pure-play” AI firm has cooled as tech giants expand offerings and competition intensifies, leaving smaller players struggling to deliver recurring growth.

If you enjoyed this summary, please drop a comment or like so we know to keep doing it in the future! Feedback is always welcomed.

Spotlight.

Last week, we released our highly anticipated 121-page, extensive research report on LVMH. LVMH is a global holding company led by Bernard Arnault that specializes in luxury goods. They own and operate over 75 “Maisons”, or brands, in six different industries from leather goods to wines to jewelry. Learn more about LVMH here!

So far this earnings season, we have released 12 2Q25 business updates. We have released business updates on Meta, APi Group, Floor & Decor, AppFolio, Coupang, Axon, Airbnb, Evolution, CoStar Group, Perimeter Solutions, Constellation Software, and DFH.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

PRM 2Q25 Business Update.

Superb Capital Allocation: “Their capital allocation continues to be superb. Perimeter deployed approximately $62mn in capital during the quarter. They invest into 3: internal capex, stock repurchases, and M&A, all of which they expect to generate a 15% or higher return on. Organic investments included $12.8 million in capital expenditures, primarily tied to production expansion in Fire Safety and Specialty. They repurchased 2.9 million shares for roughly $32 million, noting that they only opportunistically repurchase shares when they see a 15%+ IRR.”

Read the full update here: PRM 2Q25 Business Recap

CSU 2Q25 Business Recap.

Organic Growth Spark?: “While it is encouraging seeing organic growth improve, there is no reason to believe this will be their new run-rate yet. The last time organic growth was elevated, Mark Leonard attributed it to short-term factors at the AGM and it fell off shortly thereafter. We will have to wait to see if anything changed, as they have been focused on stoking organic growth for years now.”

Read the full update here: CSU 2Q25 Business Recap

LVMH Deep Dive 🧵

The Synopsis Podcast.

This week, we released a dialogue episode covering Axon’s and Coupang’s latest earnings. We break down how Axon continues to outperform expectations highlighting key growth tailwinds including AI and drones. In addition, we also unpack Coupang’s recent Cloud rebranding and its encouraging progress in Taiwan, drawing on insights from AlphaSense’s Expert Call interviews. Listen below!

*You can get a free trial of AlphaSense here

Memo of The Week.

10 Lessons From Copart’s 40 Years in Business

Copart, the global leader in online salvage vehicle auctions, has grown from a single California junkyard in 1982 to a $45bn global business, thanks to decades of disciplined strategy, innovation, and long-term ownership thinking. In this memo, we break down 10 timeless business lessons from founders Willis Johnson and Jay Adair, including: the power of aligning incentives, acting like a long-term owner, knowing when to walk away from bad bets, and turning customer service into free marketing.

Read the full memo here: 10 Lessons From Copart’s 40 Years in Business

Company Report Snippet: Floor & Decor

Direct Sourcing Advantage: “Directly sourcing also allows stronger quality control. This particularly can be an issue in the building materials industry where potential liabilities, stemming from the chemical-intensive nature of the products, can overhang for decades. Sourcing itself isn’t easy though, with FND managing 240+ suppliers in 24 different countries, who they must each give large enough orders to in order to get preferential pricing. A shortage of a product with one supplier in one country must be sourced elsewhere, requiring a fairly competent and comprehensive sourcing network. The trade war, with sporadic tariffs, only further exemplifies the value in quickly being able to move between product sources…”

*This is an excerpt from our company report on Floor & Decor.

If you are a Speedwell Research Member, read the full report here: Floor & Decor

If you are not already a Speedwell Research member, you can purchase it here: Floor & Decor Individual Report

Upcoming.

Research

We are excited to announce that we are doing an Exploratory Report on Casey’s, a convenience store and gas station chain that also happens to be the 5th largest pizza retailer in the country.

Coverage

We will be sharing a business update on Copart

RH reports earnings next week. Read our latest update on them to get up stay up to date → RH 1Q25 Business Recap

Meta, Airbnb, and Axon will be at the Goldman Sachs Communicopia & Technology Conference

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

His latest video touches on the importance of execution, using Meta, Amazon, Coupang, NVR, Old Dominion, and Constellation Software as examples.

Other Links.

A Letter a Day: Algy Smith-Maxwell Conversation With William de Gale on Investing in Technology (link)

Michael Mauboussin: Stock Market Concentration- How Much Is Too Much (link)

Aswath Damodaran: Accounting Returns, Market Returns and Good/Bad Businesses (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

Drew, I found your comment about Salesforce's Agentforce is very revealing. The adoption increased 60% Q-o-Q, but with limited revenue impact.

My wife works as a software procurement manager for an S&P 500 company, and I frequently check with her about their spending on AI tools. Her response is they have hardly spent any incremental money on AI software yet, outside some small spending on pilot projects (mostly personnel expenses). If a vendor claims they have AI functionalities and modules in the production software bundle, she would just negotiate these add-ons as freebies. She also says that they are now asking every vendor if they have AI in their tools during negotiations. If not, it would be a negative factor in their vendor selection process.

Your comment seems a confirmation of the view shared by my wife about her company. They take the AI features as a given, but are unwilling to pay or only assign a low business value at this time.

If this is also true in some other large enterprises, the revenue and ROI for the AI investment will still be years away in the future. Personally, I am very suspicious about the claims of AI revenue in many of the earnings calls I attended.